Five Things Real Estate Agents

Need To Know Before October.

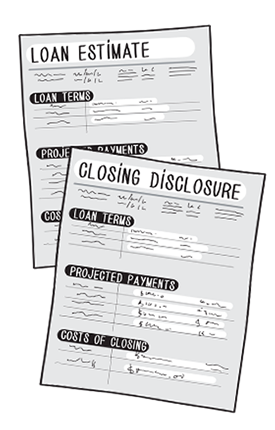

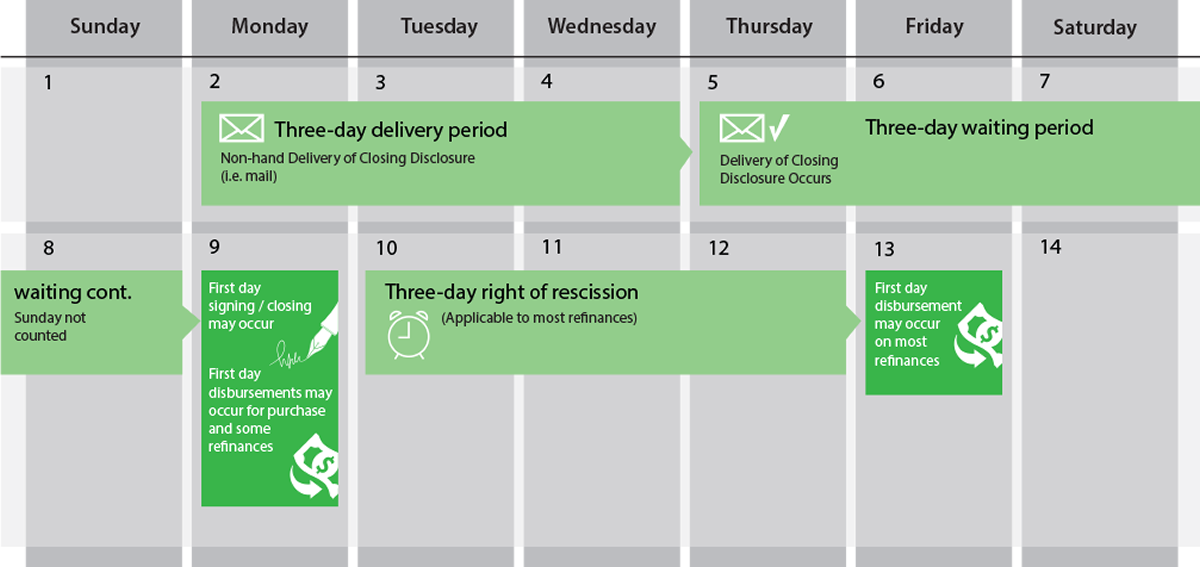

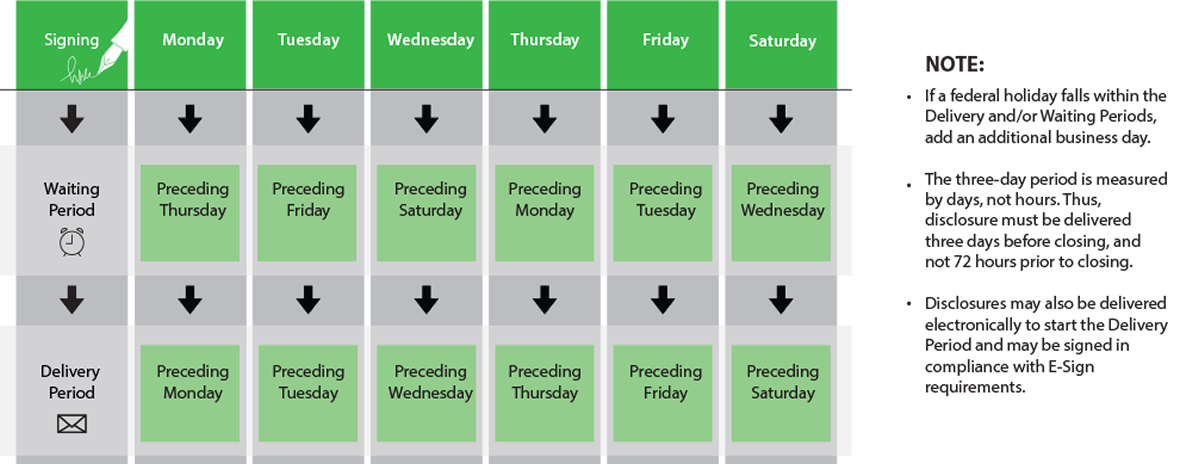

Currently, borrowers receive two separate forms from their lender at the beginning of the transaction: the Good Faith Estimate (GFE), a form required under the Real Estate Settlement Procedures Act (RESPA), and the initial disclosure required under the Truth-in Lending Act (TILA). For loan applications taken on or after October 3rd, 2015, the creditor will instead use a combined Loan Estimate form intended to replace the two previous forms. The new three-page Loan Estimate form must be provided to borrowers on a timetable similar to the current receipt of the GFE.

The combination of forms continues at the end of the transaction as well, with the HUD-1 Settlement Statement and the final TILA forms now combined into a single Closing Disclosure form. This new five-page form is used not only to disclose many terms and provisions of the loan, but also the financial transaction of the closing of the sale.

In most jurisdictions, title insurers offer a discount (often called a simultaneous-issue discount) on the loan policy premium when purchased at the same time as an owner’s policy. However, in some parts of the country, the standard purchase of an owner’s policy of title insurance is not as well established. As a result, the CFPB determined consumers were better served by showing the full, not discounted, loan policy premium in all situations on both the Loan Estimate and the Closing Disclosure instead of, where applicable, the discounted premium. If an owner’s policy is also purchased in the transaction, a formula is used to discount the owner’s policy.

In those areas where custom and practice provide that a buyer/borrower pay for both the owner’s and lender’s policies, the total actual amount paid for both policies is the same, even though the actual premium amounts are incorrect on the form.

More problematic are those areas where the seller pays for the owner’s policy and the buyer purchases the lender’s policy. In these areas, the policy premium for the lender’s policy will be overstated and the owner’s policy premium understated. As a result, look for an adjustment to be made on page 3 of the new Closing Disclosure form to correct premium amounts to those contemplated by the parties in their contract.